Opening a bank account in the US as a non-resident is possible, but it is not always simple. Many people want access to a US account because they work with American clients, study in the US, travel often, pay bills in dollars, or support family in another country. For others, the goal is more direct. They want to hold US dollars, receive international payments, or send money abroad without dealing with too many steps.

The challenge is that US banks do not all follow the same process for non-residents. One bank may ask for a US address. Another may ask for a tax identification number. Some may require you to apply in person, while others may allow part of the process online.

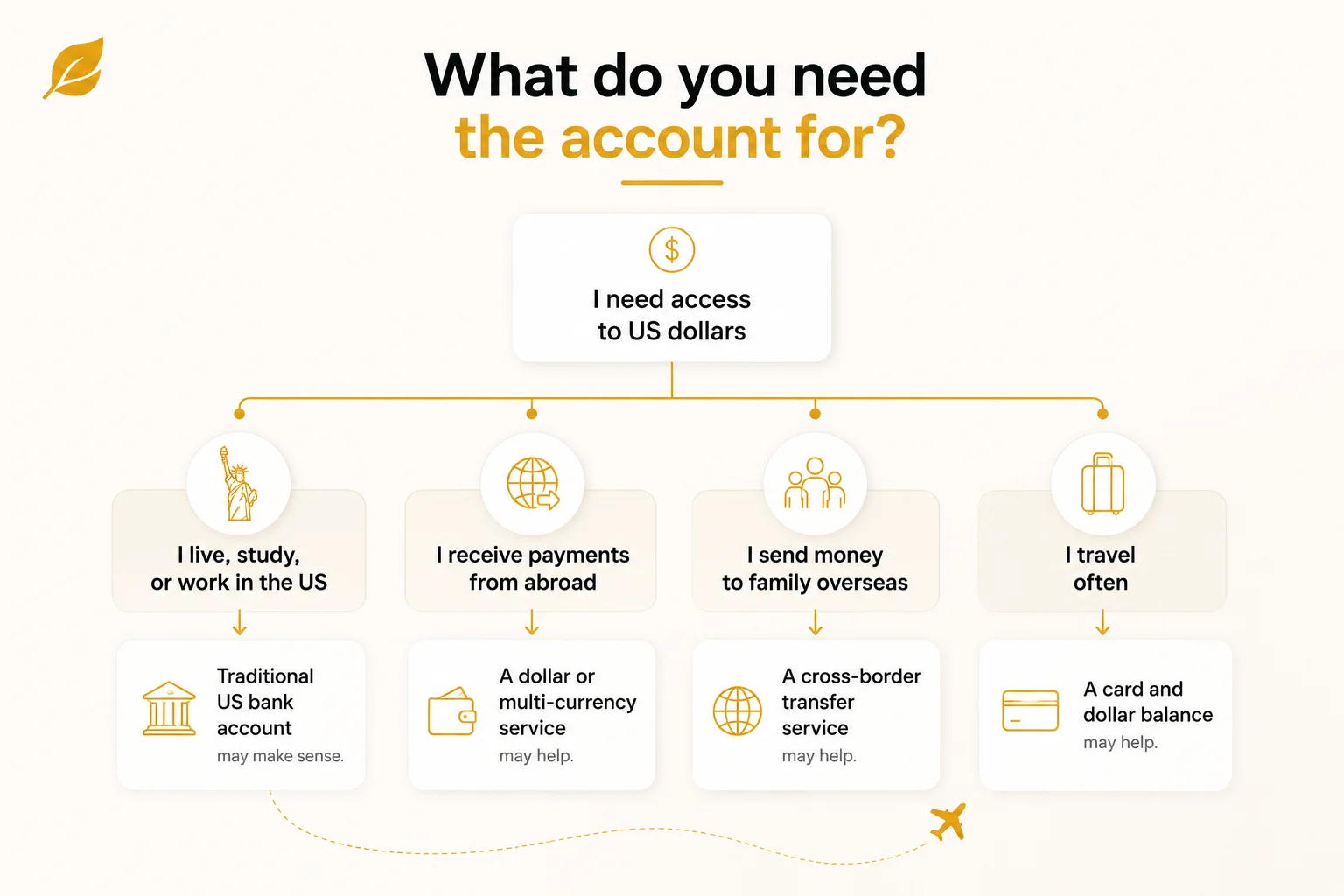

For some people, a traditional US bank account is the right choice. For others, a digital multi-currency account, foreign exchange account, or other dollar-based financial service may be easier to use.

Can a non-resident open a US bank account?

Yes, a non-resident can open a US bank account in some cases. The exact process depends on the bank, the account type, and the documents the applicant can provide.

Most banks need to verify your identity before they open an account. This is part of normal banking and compliance rules. For non-residents, this may mean showing a passport, proof of address, visa documents, and sometimes a tax identification number.

Chase Bank explains that non-residents may need identification, proof of address, and an opening deposit. It also recommends contacting the bank first because requirements can vary by institution.

This is the part people often underestimate. A bank may allow non-residents to apply, but that does not mean every non-resident will qualify. Your country, visa status, address, and documents can all affect the answer.

Why do non-residents want a US bank account?

A US account can make sense for people who have real financial ties to the country.

A student may need to pay tuition, rent, and daily expenses. A freelancer may want to receive payments from US clients. A traveler may want easier card spending during frequent visits. A family may want to hold dollars or pay bills in the US.

In many cases, the need is not really about the account itself. It is about access to dollars.

This is why some people search for an international currency bank account, multi-currency bank account, or ways to open foreign currency account services. They want a way to hold, receive, and use money in another currency without being forced through a long branch process.

These services are not always the same as a US bank account. That difference matters. But depending on your goal, they may still help you solve the main problem.

What documents you may need?

The documents you need will depend on the bank. Still, most banks will ask for some basic information before opening an account.

Passport or government ID

A valid passport is often the first requirement for non-residents. Some banks may also ask for a second form of identification.

The name on your documents should match the name on your application. If there are spelling differences, expired documents, or missing details, the bank may ask for more proof before moving forward.

Visa or immigration document

If you are in the US on a visa, the bank may ask to see your visa or immigration document.

This is common for students, workers, and people staying in the US for a longer period. A tourist may face more limits than someone with a student or work visa. The answer depends on the bank and the account type.

US address or foreign address

Address proof is one of the biggest issues for non-residents.

Some banks want a US residential address. Others may accept a foreign address, but they may ask for extra verification. A mailing address is not always the same as a residential address, so it is important to ask what kind of address the bank requires.

Do not assume that a hotel address or a friend’s address will work. If the bank asks for your residential address, it usually wants your real address.

Tax identification number

Some banks ask for a Social Security number. Others may accept an Individual Taxpayer Identification Number, also called an ITIN. Some may accept another identification number for non-US persons, depending on their rules.

The Consumer Financial Protection Bureau notes that banks and credit unions may use different identification numbers, including an SSN, ITIN, passport number with country of issuance, or alien identification card number.

This does not mean every bank accepts every option. It means you should ask before you apply.

Proof of income or account purpose

A bank may ask why you are opening the account or how you plan to use it.

This can include questions about your job, source of funds, expected deposits, or whether you plan to receive money from overseas. This is normal, especially when the account may be used for international payments.

The bank is not only opening an account. It is also checking that the account activity makes sense and follows its rules.

Can you open a US bank account online as a non-resident?

Opening a US bank account online as a non-resident can be difficult. Many traditional banks make online account opening easier for US residents because they can verify local information more easily. If you do not have a US address, Social Security number, or local documents, the online application may stop before you can complete it.

Some banks may let you begin the application online but ask for in-person verification later. Others may require you to visit a branch from the start.

There are also digital providers that offer access to dollar balances, international transfers, or card services online. These can be easier to use, but users should understand what they are applying for. A financial technology company may offer bank-like services, but it may not be a chartered bank.

This does not mean the digital option is bad. It simply means users should know who provides the service, what protections apply, and what countries are supported.

Do you need an SSN to open a US bank account?

You do not always need a Social Security number to open a US bank account, but not having one can limit your options.

Some banks require an SSN. Some may accept an ITIN. Others may accept different identification documents for non-US persons, depending on their policies and the account type.

The FDIC has guidance on customer identification requirements. For a non-US person, identifying information may include a taxpayer identification number, passport number and country of issuance, alien identification card number, or another government-issued document showing nationality or residence.

The important point is that the bank must be able to identify you. If you do not have an SSN or ITIN, you should ask the bank what other documents it accepts before applying.

Can you open a US bank account without a US address?

Some banks may allow it, but many will make the process harder without a US address.

A bank may ask for a US residential address, a mailing address, or both. Some banks may accept a foreign address if you can prove it. Others may require a US address before they will open the account.

This matters because banks need to know where their customers live. They may also need an address for statements, tax documents, debit card delivery, and compliance checks.

If you only have a foreign address, ask the bank whether it accepts non-resident applicants and what proof it needs. It is better to ask before you start than to get stuck halfway through the application.

What if you only need to hold or use dollars?

Not everyone who wants a US account needs full US banking.

Some people mainly want to hold dollars, receive money from overseas, make international payments, or send money abroad. If that is the case, a different type of account may be enough.

A digital multi-currency account, foreign exchange account, or international currency bank account can help some users hold and manage more than one currency. Depending on the provider, it may also help with transfers, card use, or receiving payments from another country.

This can be useful for freelancers, travelers, students, and people who support family across borders.

Still, it is important to be clear. A multi-currency service is not always the same as a US bank account. It may not offer the same protections, account features, or legal status. Before choosing one, check what the provider offers, where it works, what fees apply, and how your money is held.

How to choose the right option

The right option depends on your actual need.

Start with your real need

Before applying anywhere, be clear about why you want the account.

If you live, study, or work in the US, a traditional bank account may make sense. It can help with salary, rent, tuition, card payments, and local bills.

If you live outside the US and mainly need dollar access, a digital account or multi-currency service may be easier. It may help you hold USD, receive funds, convert currencies, or send money internationally without going through a full US bank account process.

Check document requirements

Do not start the application until you know what documents are needed.

Ask whether the provider needs a passport, visa, proof of address, tax identification number, opening deposit, or in-person visit. If one document is missing, your application may be delayed or rejected.

Check where the service works

A provider may support US dollars but not operate in your country. Another may let you receive funds but not send them to the countries you need. Before choosing, check supported countries, currencies, and transfer routes.

Check how money can be received and sent

Make sure the account supports the way you actually use money.

Can you receive funds from clients, family, or platforms? Can you send money to the countries you need? Are there transfer limits? Can you use a card? Can you hold more than one currency?

These details matter more than the name of the account.

Check safety and account protection

If the provider is a bank, check whether it is FDIC-insured. The FDIC says deposit insurance protects money at FDIC-insured banks up to at least $250,000 per depositor, per insured bank, for each ownership category.

If the provider is not a bank, check what protections apply and which licensed partners are involved. A bank-like service can still be useful, but users should understand how it works before relying on it.

Is a US bank account the best option for non-residents?

A US bank account can be useful, but it is not always the best or easiest option. It may be the right choice if you are studying, working, renting, or spending regularly in the US. It may also help if you need a local US account for bills or direct payments.

But if your main goal is to hold dollars, get paid internationally, travel, or support family abroad, a bank-like digital service like PureFi may be what you need. It can give you the access you need without the same branch visits or paperwork.

The best choice is the one that fits your documents, country, currency needs, and daily use. A traditional account can be helpful, but it is not the only way to manage money across borders.

Conclusion

Opening a US bank account as a non-resident is possible, but it depends on more than your passport. Your address, tax identification number, visa status, and bank choice can all affect the process.

Before applying, be clear about what you need. If you need full US banking, a traditional account may be worth the effort. If you mainly need dollar access, international payments, or a way to send and receive money across borders, another option may be easier.

Get PureFi for money transfers

PureFi helps you send money abroad for less, with clear fees and a simple way to hold and grow your money. We use new technology to make cross-border transfers faster, fairer, and more transparent.

Learn more about how PureFi can help you send, save, and grow money across borders, or download the app to get started today.