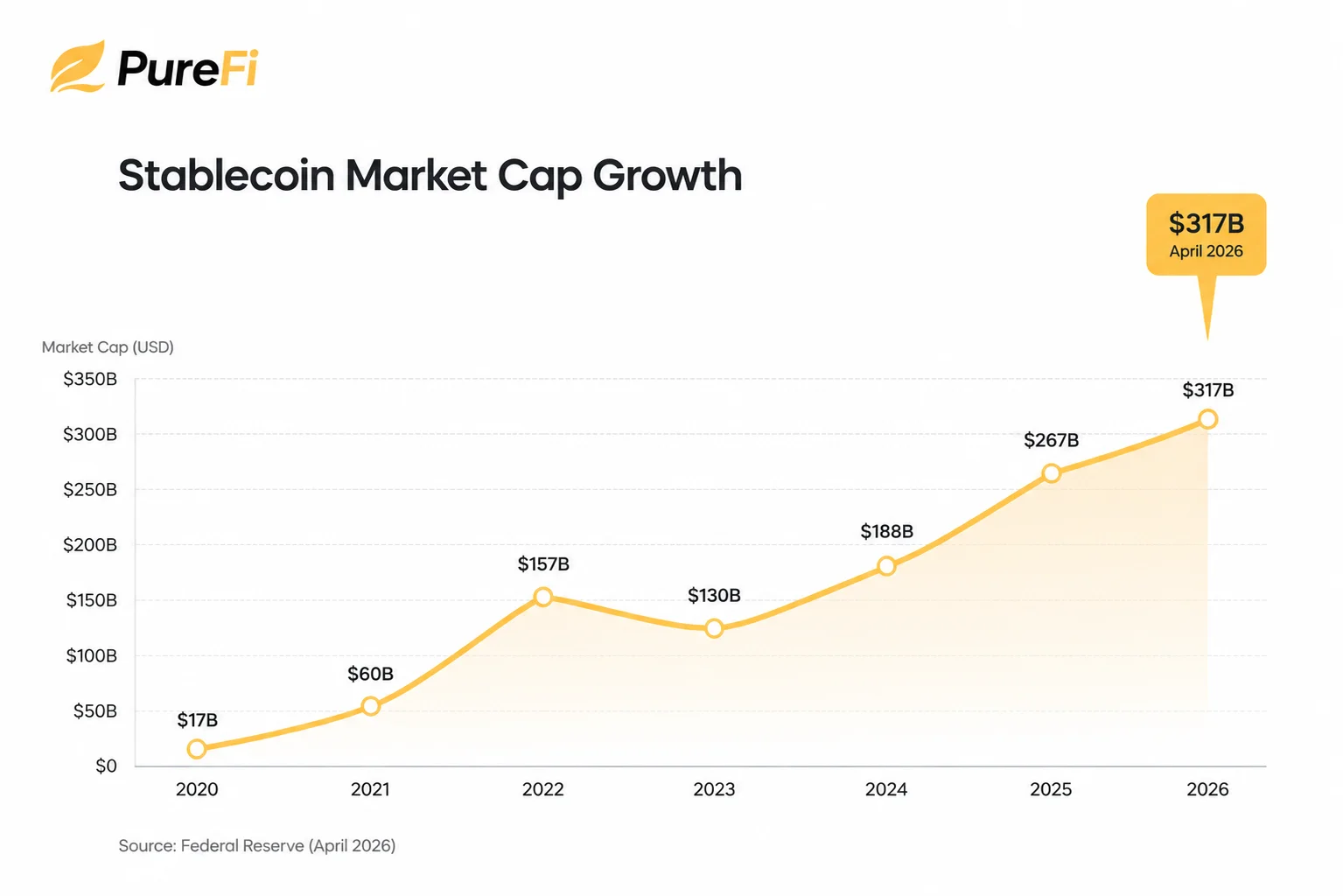

Stablecoins started as a crypto-native product, but they are now part of how money transfers across borders. Businesses use them to settle supplier payments, pay contractors in markets with limited access to banking, hold dollar-backed value, and transfer funds outside traditional banking hours.

That speed is useful, but it also comes with responsibility. A stablecoin is only as strong as the reserves, issuer, regulation, custody setup, and redemption process behind it. A well-backed coin with clear reporting can behave close to digital cash. A coin with weak disclosures, poor oversight, or an unstable design can quickly lose trust.

So when people ask whether stablecoins are safe, we think the better question is: safe for what, held where, and backed by whom?

What is a Stablecoin?

A stablecoin is a digital token designed to follow the value of another asset. In most cases, that asset is the U.S. dollar. So, when people talk about a dollar stablecoin, they usually mean a token designed to track $1 closely.

The Federal Reserve describes stablecoins as tokens that aim to maintain a stable value by pegging to a real-world reference asset, such as the U.S. dollar. That is the basic idea. Instead of holding a cryptocurrency that may rise or fall sharply in a day, a user holds a digital version of a dollar that can be transferred across blockchain rails.

Now that does not automatically make every stablecoin the same. The design, issuer, reserves, regulation, and redemption process all matter. But at the simplest level, a stablecoin is meant to make digital money easier to use without the constant price swings people associate with crypto.

Why Do Stablecoins Exist?

Stablecoins exist because most cryptocurrencies are not practical for everyday payments. If a token’s price can transfer 5%, 10%, or more in a short window, it becomes hard to use for salaries, invoices, remittances, or savings. You don’t want to send $500 to a family member and have it arrive with a different value because the market moved.

Stablecoins were built to solve that problem. They give users a digital asset that can be transferred quickly, often outside normal banking hours, while still tracking a familiar currency. This is why they are used for trading, payments, transfers, liquidity management, and holding digital dollars.

The 24/7 nature matters. Visa’s on-chain analytics show stablecoin transaction activity continues through weekends, with weekend volumes averaging billions of dollars. Traditional banking rails were not designed for that kind of always-on movement.

Why Most Stablecoins are Linked to the U.S. Dollar?

Most stablecoins are tied to the U.S. dollar because global demand for it is already high. The dollar is used in trade, savings, invoices, imports, exports, and cross-border payments. Federal Reserve Governor Christopher Waller noted that the U.S. dollar is the fiat currency of choice for most stablecoins.

This matters most for people without easy access to dollars. Freelancers may want to receive international payments in dollars. Immigrants may want to send money home without incurring too many fees or exchange-rate spreads. Families in countries with weaker currencies may want to hold part of their money in a more stable currency.

Stablecoins are especially appealing for users in countries with high inflation, capital controls, or limited access to dollar accounts. That is the real reason stablecoins have moved beyond crypto trading.

So, are Stablecoins Safe?

Simply put, stablecoins can be safer than volatile crypto, but they are not the same as insured bank deposits. That is where most of the confusion starts.

People hear “stable” and assume it means risk-free. It does not. It means the coin is designed to track the value of something else, usually the U.S. dollar. Whether it actually does that well depends on what is sitting behind it.

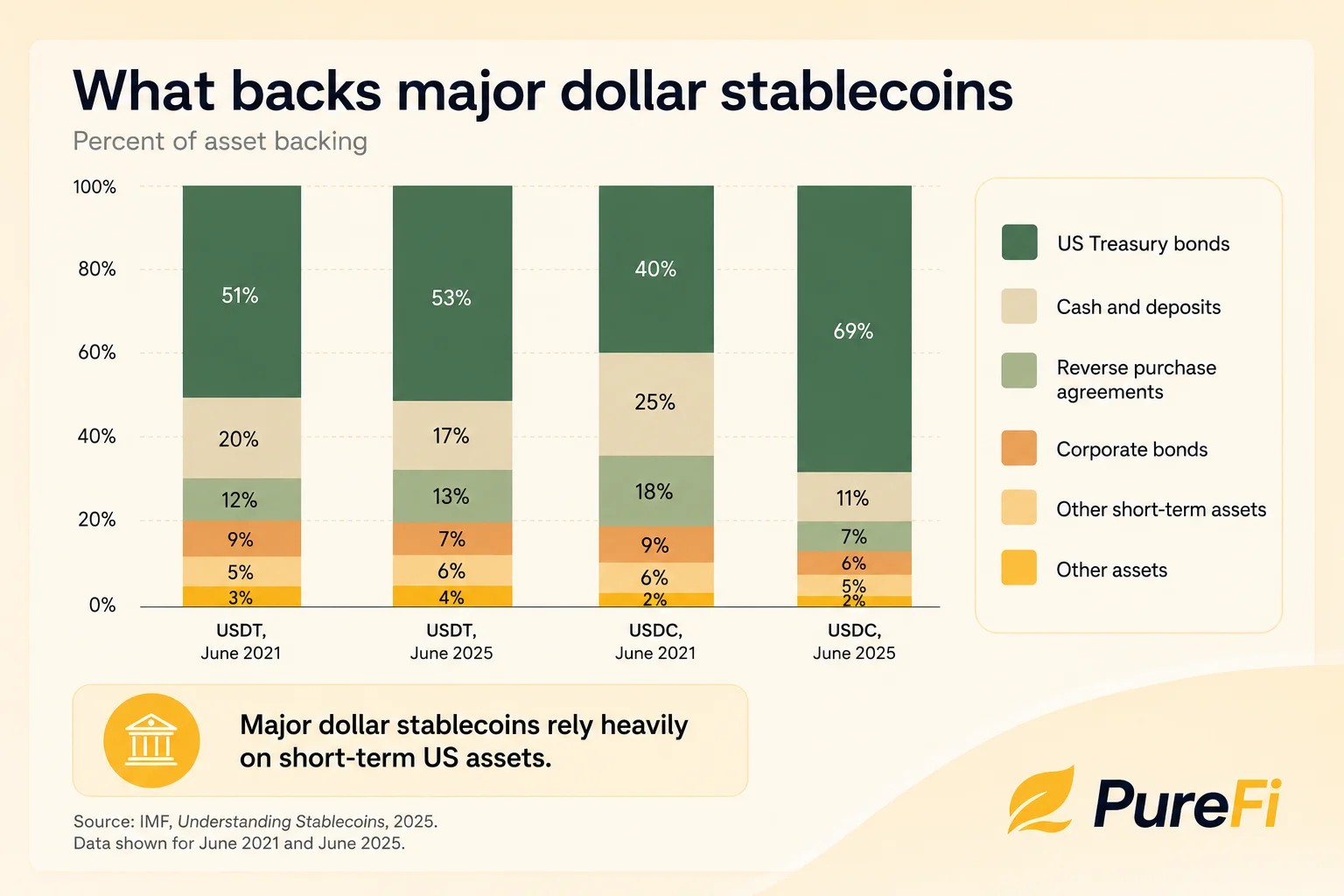

A fiat-backed stablecoin with clear reserves and regular reporting is very different from an algorithmic stablecoin that depends on market demand to hold its price. Stablecoins can be backed in different ways, including by traditional assets, crypto assets, or algorithms.

Safer than Bitcoin does not mean risk-free

To be honest, comparing stablecoins to Bitcoin only answers one part of the question. Yes, stablecoins are designed to avoid the price swings Bitcoin is known for. But price is not the only thing that matters.

We also have to look at reserves, redemptions, custody, regulation, and the platform that holds the funds. If the reserves are unclear, or users cannot redeem the coin when they need to, the word “stable” starts to lose meaning.

So we do not judge a stablecoin by the peg alone. We look at what backs it, who controls it, and what happens when the market is under pressure.

The 5 Main Risks of Stablecoins

We don’t believe stablecoins are scary by default. But we also don’t think the word “stable” should make anyone switch off their judgment. The risks are real, and they usually sit behind the scenes.

1. Reserve Risk

A stablecoin is only as reliable as what backs it. If the issuer says every coin is worth $1, users should be able to understand where that $1 sits. Is it in cash? Short-term Treasuries? Bank deposits? Something harder to sell?

This matters because weak or unclear reserves can quickly become a confidence problem.

2. Redemption Risk

The real test comes when many people want their money back at the same time. In March 2023, USDC temporarily lost its peg after Circle disclosed that part of its reserves were held at Silicon Valley Bank, which had failed. The Federal Reserve later described how that announcement triggered a rush of redemptions and pressure in secondary markets.

3. Depeg Risk

A depeg simply means the coin stops trading at its intended value. Sometimes that transfer is temporary. Sometimes it is not. The Terra-Luna collapse showed how badly things can break when a stablecoin depends on fragile market incentives instead of clear reserve backing.

4. Custody and Platform Risk

Even if the stablecoin itself is well-backed, the platform holding it still matters. Users need to know who controls access, where assets are stored, what happens during a platform outage, and whether withdrawals are available when markets are stressed.

5. Yield Risk

This is the part people often skip. If a stablecoin product offers yield, that yield is coming from somewhere. It may come from lending, Treasuries, DeFi markets, real-world assets, or other strategies. Higher returns are not inherently bad, but they should always prompt better questions.

Are Stablecoins Legally Recognized for Business Use?

Stablecoins are not legal tender in most markets. They are not issued by central banks, and businesses should not treat them the same way they treat national currency. But in many countries, businesses can still use stablecoins under crypto, payments, tax, AML, and sanctions rules.

- In the U.S., the GENIUS Act created a federal framework for payment stablecoins and limits issuance to permitted issuers.

- In the EU, MiCA sets rules for crypto-asset issuers and service providers.

- In Singapore, regulators have finalized a stablecoin framework covering reserves, redemption, and disclosure.

The picture is still uneven. China continues to ban virtual currency activity, including stablecoins. Brazil now treats some fiat-pegged virtual asset transactions as foreign exchange operations. Nigeria has rules covering digital assets, custodians, exchanges, and VASPs.

So, simply put, businesses can use stablecoins in many markets, but not casually. The legal space is getting clearer, but local rules still matter.

What Industries Benefit the Most from tablecoins?

Stablecoins make the most sense in industries where money often has to transfer across borders quickly and with fewer intermediaries. They are less exciting for businesses that only pay local vendors in one currency. The real value shows up when time zones, banking delays, exchange-rate spreads, and limited access to dollars become part of daily operations.

Cross-Border Payments and Remittances

This is the obvious one. Global remittance costs are still high. The World Bank’s Remittance Prices Worldwide tracker shows the global average cost of sending remittances was 6.36%. For families and businesses moving money often, that cost adds up fast.

Freelance and Contractor Payments

Stablecoins can also help companies pay contractors in underbanked markets. A freelancer may not have easy access to a dollar account, but they may still want to receive dollar-linked value for international work. This is where stablecoins become less of a crypto story and more of a payroll and access story.

Import, Export, and Supplier Payments

For businesses paying overseas suppliers, stablecoins can reduce settlement delays and make payments easier to track. BIS notes that stablecoins can be appealing for firms that face restrictions in accessing dollar-based international payment networks, especially for cross-border payments and trade settlement.

Fintechs and Global Platforms

Fintech apps, marketplaces, and global platforms can use stablecoins as payment infrastructure in the background. The end user may not even think about the blockchain layer. They just see faster movement, dollar-backed balances, and fewer delays.

Treasury and Liquidity Management

Stablecoins can also help companies treanfer funds outside banking hours. Visa’s stablecoin analytics shows that activity continues through weekends, with weekend transaction volumes averaging billions of dollars. For businesses managing global liquidity, that always-on movement can be useful.

How PureFi Can Help

PureFi gives users a simpler way to send, hold, and grow money across borders. You can send international transfers, see the exchange rate and fee before you pay, and choose payout methods such as bank deposit or mobile wallet, where available. PureFi supports transfers to 90+ countries.

PureFi can help you:

Send money with more clarity: Check the exchange rate, transfer fee, and final amount before sending to avoid surprises at the last step.

Hold digital dollar value: Keep money in a stablecoin-backed account instead of moving in and out of traditional banking rails every time you need to send funds.

Earn while your balance rests: PureFi targets 6% APY on eligible balances, with earnings shown in-app. The rate is variable, and actual returns may change based on the performance of the yield source.

Transfer money across borders faster: Send money internationally through a digital onboarding and transfer flow built for users who support family, pay globally, or manage money between countries.

Use stablecoins without handling the complexity yourself: PureFi is built to make stablecoin-backed finance feel more practical, with upfront pricing, transfer tracking, and a user experience that doesn’t require you to manage crypto tools yourself.

Learn more about how PureFi can help you send, save, and grow money across borders, or download the app to get started today.