For decades, sending money across borders has depended on a system built for banks, not everyday people. A simple transfer can pass through several providers before reaching the person on the other end. Each step can add time, fees, or a weaker exchange rate.

Stablecoins change the path. They let people send dollar-linked value via newer payment rails that settle faster and with fewer intermediaries. That can lower costs, especially for people who often send money abroad.

We still have to be honest about the limits. Stablecoin transfers are not always free. Local payout fees, cash-out costs, platform charges, and exchange rates can still apply. The benefit is that the process can be cleaner and easier to price.

Below, we’ll explain why traditional cross-border payments cost so much, and how stablecoins can reduce what users lose along the way.

What are stablecoin cross-border payments?

A stablecoin cross-border payment is a transfer of digital value designed to track a real currency, usually the U.S. dollar.

For the user, the idea is simple. You send dollar-linked value from one country to another through a digital platform. The receiver may keep that value, convert it, or receive it through a local payout method, depending on the service and country.

The technical part sits in the background. People don’t need to study payment rails to care about this. They care about the real questions:

- How much will I pay?

- What rate will I get?

- How much will my family receive?

- How long will it take?

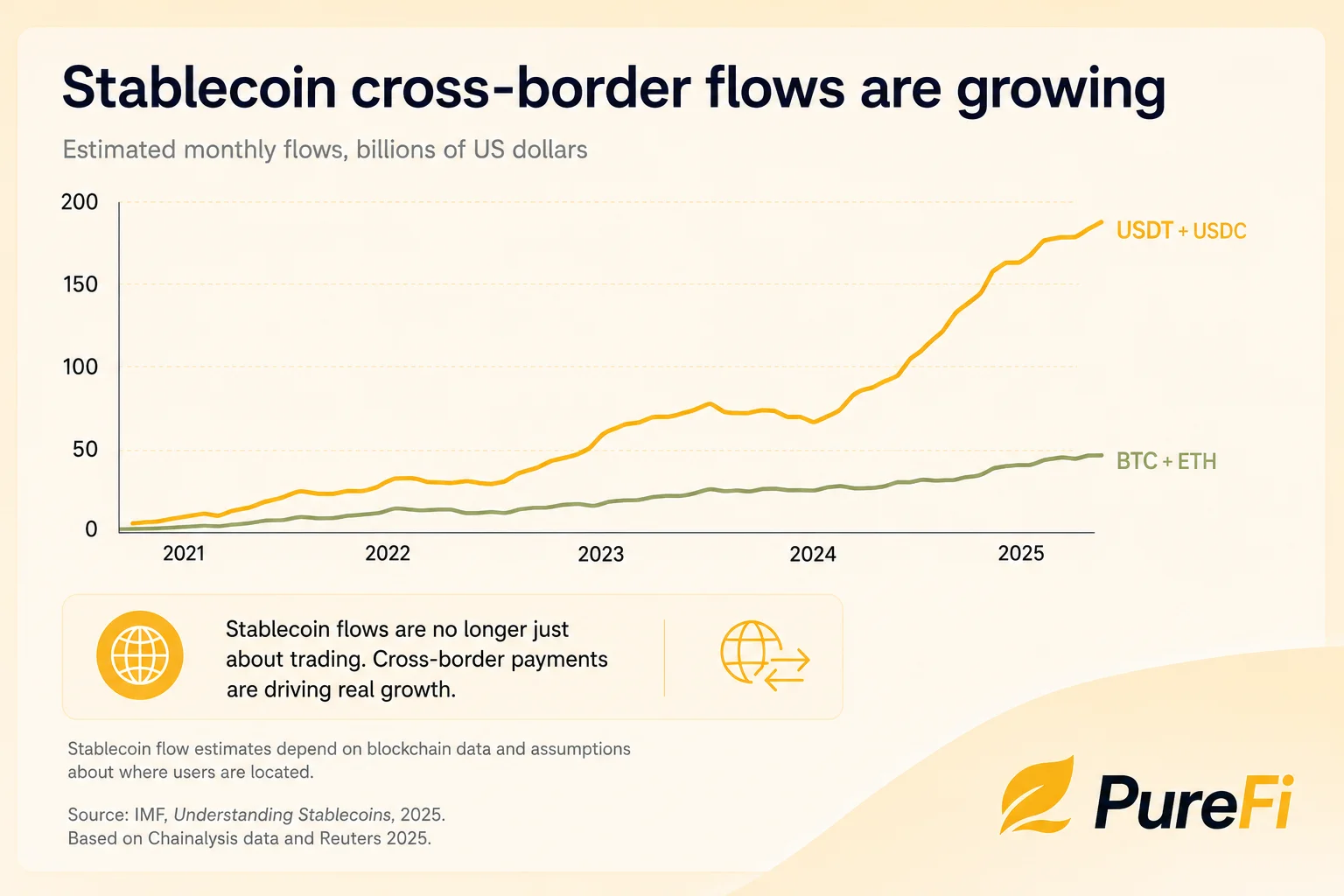

Cross-border payments are often slower, more expensive, and less clear than local payments. It also explains that payment stablecoins may reduce reliance on some intermediaries in cross-border transactions. That is the main reason stablecoins matter here; they can help reduce the number of paid steps between sender and receiver.

Why are cross-border transactions expensive?

Cross-border transfers are expensive because the fee you see is not always the full cost. A transfer can include the upfront fee, a weaker exchange rate, bank charges, and payout costs. The World Bank says the global average cost of sending remittances is 6.36% of the amount sent.

| Payment method | Transfer fee | Currency conversion cost | Other charges | Total cost |

|---|---|---|---|---|

| Bank transfer | $30 to $50 | Often included in the exchange rate | $10 to $30 | $40 to $80+ |

| Card or payment app | Often percentage-based | May include a markup | Varies by provider | Varies |

| Cash pickup transfer | Upfront fee | May include a markup | Possible pickup charges | Varies |

| Stablecoin-based transfer | Usually lower platform cost | Clearer when conversion happens | Cash-out or payout fees may apply | Depends on route |

The point is not that stablecoin transfers are always free. They aren’t. The point is that they can reduce some of the layers that make traditional transfers expensive. A good platform should show the fee, the rate, and what the receiver gets before you send.

5 ways stablecoin payments can reduce fees

1. They can reduce the extra middle layers

The old system often requires multiple providers to complete a single international transfer. Each provider has its own cost. That is one reason sending money abroad can feel more expensive than it should.

Stablecoins can create a shorter payment path. In many cases, the sender and receiver do not need the same number of banks or settlement partners in the middle. This does not mean every cost disappears. A platform may still charge a fee. Local payout may still cost something. But fewer paid steps can make the full transfer cheaper and easier to understand.

2. They can lower the cost of settlement

Settlement is the process by which payment is completed between the parties involved. With traditional transfers, settlement can take time because banks and payment systems may work on different schedules. Weekends, holidays, and country cut-off times can all slow things down.

Stablecoins can settle via digital rails that operate outside normal bank hours. BIS research notes that cross-border payments, including remittances and retail payments, remain slower, costlier, and harder to access than they should be.

When settlement is faster, providers may not need to carry the same delay cost. For users, that can mean lower fees and fewer waiting problems.

3. They can make exchange costs clearer

Many people think the transfer fee is the whole cost. It often isn’t. A provider can show a low fee and then offer a weaker exchange rate. The sender may think they saved money, but the receiver gets less. This is one reason people search for how to avoid currency conversion fees.

Stablecoin payments can make this clearer because the dollar-linked value is easier to show before the receiver converts it into local currency. The platform can separate the transfer fee from the currency conversion cost.

4. They can make smaller transfers more practical

Small transfers can be hit hardest by fixed fees. If someone sends $50 and pays a $5 fee, that is 10% gone before the receiver gets anything. For families who send smaller amounts often, this adds up.

Stablecoins can make smaller cross-border transfers more practical because the cost structure can be lighter than older bank-based routes. This is useful for family support, gifts, shared bills, and regular help sent from abroad.

We think this is important. A fair system should not punish people for sending smaller amounts.

5. They can reduce the cost of waiting

Delay has a cost, even when it does not show up as a fee. If money arrives late, a family may miss a payment, borrow from someone else, or pay extra charges. A freelancer may wait longer to use the money they earned. A student may not get funds when school fees are due.

Stablecoin transfers can help because they are built for faster settlement. The FSB’s G20 roadmap exists because global leaders have recognized that cross-border payments need to become faster, cheaper, more transparent, and more inclusive.

Speed is not only about convenience. In real life, faster access can protect people from extra costs.

How can individuals use stablecoins in their payments?

The safest starting point is to use a trusted platform that clearly explains the full cost. Users should not have to manage technical tools or guess where the money is going. Before using stablecoins for personal payments, we’d consider a few simple factors.

First, check the fees before sending. The platform should show what you pay and what the receiver gets. Second, check the exchange rate. A low transfer fee does not always mean a low total cost. Third, understand how the receiver can use the funds. Can they receive through a local account, mobile wallet, or another payout method?

It also helps to start small. Send a lower amount first, check the timing, check the final amount, and make sure the receiver understands the process. This is not financial, tax, or legal advice. It is basic safety. New payment tools can be useful, but people should still know what they are using and what it really costs.

Conclusion

Stablecoins can reduce transaction costs by changing how cross-border transfers are processed. They can cut extra middle layers, support faster settlement, clarify exchange costs, and make smaller transfers more practical.

That does not mean every stablecoin transfer is cheap or safe by default. The platform matters. The payout method matters. The fees, rate, country rules, and user experience all matter.

But the old system has a clear problem. It often overcharges and underserves the same people who rely on remittances the most. We believe better tools should help people send money abroad for less, see the cost upfront, and keep more of what they earn.

Get PureFi for money transfers

PureFi helps you send money abroad for less, with clear fees and a simple way to hold and grow your money. We use new technology to make cross-border transfers faster, fairer, and more transparent.

Learn more about how PureFi can help you send, save, and grow money across borders, or download the app to get started today.