Sending money abroad should be simple. In many cases, it still isn’t.

A person may send $500 to family and lose part of it to transfer fees, exchange rate markups, bank deductions, or pickup charges. The sender may not know the full cost until the money is already on its way. The receiver may wait for days, especially if banks are closed, or a payment passes through several intermediate layers.

This is why stablecoins are getting attention in international remittance. They can help money transfer faster, often at a lower cost, and with more control for the sender and receiver.

Now, stablecoins don’t fix every problem. They also need clear rules, safe platforms, and honest pricing. But when used correctly, they can make cross-border payments fairer for people who already give up too much to send money home.

What is a stablecoin?

A stablecoin is a digital token made to follow the value of another asset. Most stablecoins are linked to the U.S. dollar. That means one dollar-backed stablecoin is designed to stay close to $1.

This is different from other digital assets that can rise or fall a lot in a short time. For remittances, that matters. A family sending school fees, rent, or medical support doesn’t want the value to change before the money arrives.

The Federal Reserve explains that a payment stablecoin is designed to be used for payments, with rules intended to help keep its value stable against the U.S. dollar.

In simple terms, stablecoins help people transfer dollar-linked value using newer payment rails. The user doesn’t need to care about the technical layer. They care about the outcome: send money abroad for less, move it faster, and keep more of what they earn.

1. Lower transfer costs

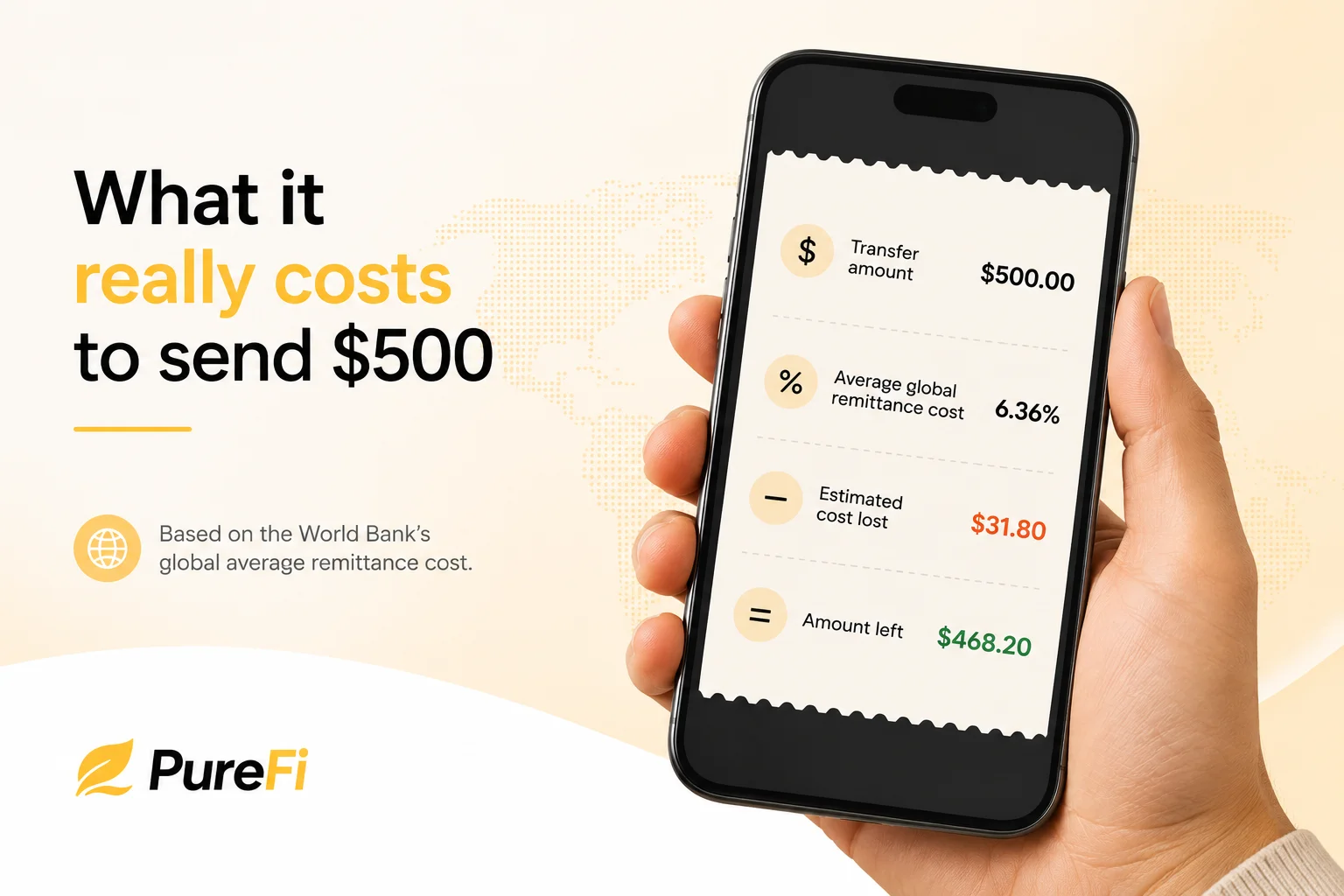

The first benefit is cost. This is also the easiest one to understand.

The World Bank says the global average cost of sending remittances is 6.36% of the amount sent. That means a $500 transfer can incur more than $30 in fees before it reaches the recipient, depending on the route and provider.

Stablecoins can reduce some of that cost because they don’t always need the same long chain of banks, processors, and middle layers. That does not mean every stablecoin transfer is free. There can still be platform fees, cash-out fees, or exchange costs. But the model can make pricing more direct.

For us, this is one of the clearest reasons stablecoins matter. If a person works hard to send money home, they should know what it really costs.

2. Faster money movement

Many traditional transfers still depend on bank hours, cut-off times, holidays, and settlement delays. That can be painful when the money is for rent, food, school, or an emergency.

Stablecoins can move outside normal banking hours. Visa’s stablecoin data shows that stablecoin activity continues through weekends, with weekend transaction volumes averaging billions of dollars per day.

That speed does not remove every delay. A user may still need time to add funds, verify their account, or cash out into local money. But the transfer layer itself can be much faster than the old way.

For international remittance, faster payment can be the difference between helping today and helping three days later.

3. More transparent fees

Hidden fees are one of the biggest problems in money transfer. A provider may show a single transfer fee and then make money on the exchange rate. Or the receiver may get less because another bank deducted charges along the way.

Stablecoin payments can make the movement of funds easier to track. The sender can often see the amount being sent, the route, and the cost before confirming. That can help users who want to know about how to avoid currency conversion fees they did not expect.

This does not mean every provider is honest. A platform can still add fees around the transfer. But stablecoins give fintech companies a better way to build clearer pricing. A fair service should show people the fee, the rate, and the amount the receiver gets before the transfer is sent.

4. Better access to dollar-linked value

In many countries, people want access to U.S. dollars but cannot easily open a dollar account. Others live with high inflation, weak local currency, or strict limits on foreign currency access.

The Bank for International Settlements notes that stablecoins can give users access to foreign currencies, mostly the U.S. dollar. It also says they may appeal to people and businesses in countries with high inflation, capital controls, or limited access to dollar accounts.

This is a major reason stablecoins matter for remittances. A receiver may not want to convert the full amount right away. They may want to keep part of it in dollar-linked value and use it later.

5. Easier payments for people without strong bank access

Many remittance receivers do not have full access to banking services. Some use mobile wallets. Some rely on cash pickup. Some have a bank account, but it may not be easy or cheap to receive money from abroad.

The World Bank’s remittance database tracks costs across 377 country corridors from 48 sending countries to 111 receiving countries. That shows how large and complex the remittance system still is.

Stablecoins can help create more ways to receive value, especially when paired with local payout methods. The receiver may not need to depend only on one bank route. Access depends on local rules and available partners. But the direction is promising. New payment tools can reach people that the traditional system has not served well.

6. More control for senders and receivers

When money moves through the old system, users often feel like they lose control. They send the money, then wait. If there is a delay, it can be hard to know where the payment is or who is holding it.

Stablecoin-based transfers can make the process more visible. Users can often track movement more clearly and see when funds are sent or received. This is useful for families, but also for freelancers, small businesses, and people who receive support from abroad.

Control also means choice. A receiver may choose when to convert. A sender may choose when to send. A platform may show fees before payment. These small things make a big difference when people are sending money often.

Better control is part of making money work for people, not against them.

7. Useful for freelancers and global workers

Remittances are not only family transfers. Many people now work for clients in other countries. They may be freelancers, remote workers, contractors, or small business owners.

For them, receiving money from overseas can be slow and expensive. Some platforms take a cut. Some banks charge to receive international payments. Exchange rates may not be clear.

Stablecoins can help workers receive dollar-linked value faster, especially in markets where international payment options are limited. The IMF has noted that stablecoins may provide firms and individuals in emerging markets with easier access to foreign currency, especially where local currencies are weak or inflation is high.

8. Helpful for small businesses and supplier payments

Small businesses also feel the pain of cross-border payments. Paying a supplier in another country can be slow. The fees may be unclear. The exchange rate may change. The payment may pass through more than one bank.

BIS research says cross-border payments, especially remittances and retail transactions, remain more costly, slower, and less accessible than they should be.

Stablecoins can help businesses move value faster and with fewer steps. This is useful for importers, online sellers, service businesses, and firms that pay global contractors.

Of course, businesses need strong records, local compliance checks, and clean accounting. Stablecoins do not remove that work. They just give businesses another way to move money when the old way is too slow or too costly.

9. More support for 24/7 global life

Money does not only need to be transferred from Monday to Friday. A parent may need funds on a Sunday. A freelancer may need to wait to be paid after a client in another time zone sends payment. A business may need to settle an invoice when banks in one country are closed.

This is where stablecoins fit modern life. They are built for always-on movement. Visa says its dashboard tracks stablecoin movements across major networks to show trends in supply and transaction volume.

That always-on nature is one of the top benefits of stablecoins for remittances. It matches how people live now. Families, workers, and businesses do not stop needing money because a bank is closed.

10. A better base for fair financial tools

The biggest benefit may not be one transfer. It may be what stablecoins make possible around the transfer.

They can support digital dollar balances, international payments, clearer pricing, faster settlement, and tools that help users grow their money without predatory interest. They can also help fintech companies build services for people who have been overcharged or underserved by the traditional system.

Stablecoins are not a cure for every problem in finance. They need clear rules, safe providers, good reserves, and honest communication. The World Bank has also warned that stablecoin projects are not a cure-all for cross-border payments and may pose new risks if not handled well.

But used responsibly, they can help build a fairer way to send and receive money across borders.

Conclusion

Stablecoins matter for remittances because they speak to real problems. People want to send money abroad for less. They want faster transfers, fewer hidden fees, dollar-linked value, and a safer way to support family, pay workers, and move money across borders.

The old system often makes this harder than it needs to be. It overcharges people who can least afford it, adds delays when time matters, and hides costs inside exchange rates and middle-layer fees.

Stablecoins can help change that, but only when they are used with care. The safest way to transfer money is about speed and price, but also about trust, rules, transparency, and knowing what happens to your money at every step.

At Purefi, that is the standard we believe users deserve.

Get PureFi for money transfers

PureFi helps you send money abroad for less, with clear fees and a simple way to hold and grow your money. We use new technology to make cross-border money transfers faster, fairer, and more transparent.

Learn more about how PureFi can help you send, save, and grow money across borders, or download the app to get started today.