You don’t have to be on vacation to pay a foreign transaction fee. It can happen when you book a hotel in another country, buy from an overseas website, pay for a travel app, subscribe to a service billed in another currency, or use your card at dinner while abroad.

The price may look fine at checkout. Then your statement shows a little extra. That extra charge is usually small, often around 1% to 3%. But small fees add up, especially if you travel, shop across borders, or support family in another country.

People should know what they’re paying before the charge appears. When money crosses borders, the full cost should be clear. That means the card fee, the exchange rate, and the final amount.

What is a foreign transaction fee?

A foreign transaction fee is an extra charge added when your card payment is processed outside your home country or in another currency.

You may see it when you use your card while traveling. You may also see it when you buy from a foreign website, pay for a hotel abroad, use an overseas ATM, or subscribe to an app that bills you in another currency.

The confusing part is that the business may not feel foreign. A website can look local, show prices in your currency, and still process payments through a bank in another country. That can trigger the fee.

This type of fee may apply when you use a card in another country or make an international purchase. It is usually charged as a percentage of the transaction amount.

How much is a foreign transaction fee?

Foreign transaction fees often range from 1% to 3% of the purchase amount. The fee can apply to purchases made in foreign currency or processed through non-U.S. banks.

Here’s a simple example.

If you spend $500 and your card charges a 3% foreign transaction fee, you pay $15 extra.

That may not feel like much once. But if you pay that kind of fee every month, it becomes $180 in one year. The first price you see is not always the final price you pay.

Why do banks charge foreign transaction fees?

Banks and card providers may charge foreign transaction fees because international card payments need extra processing.

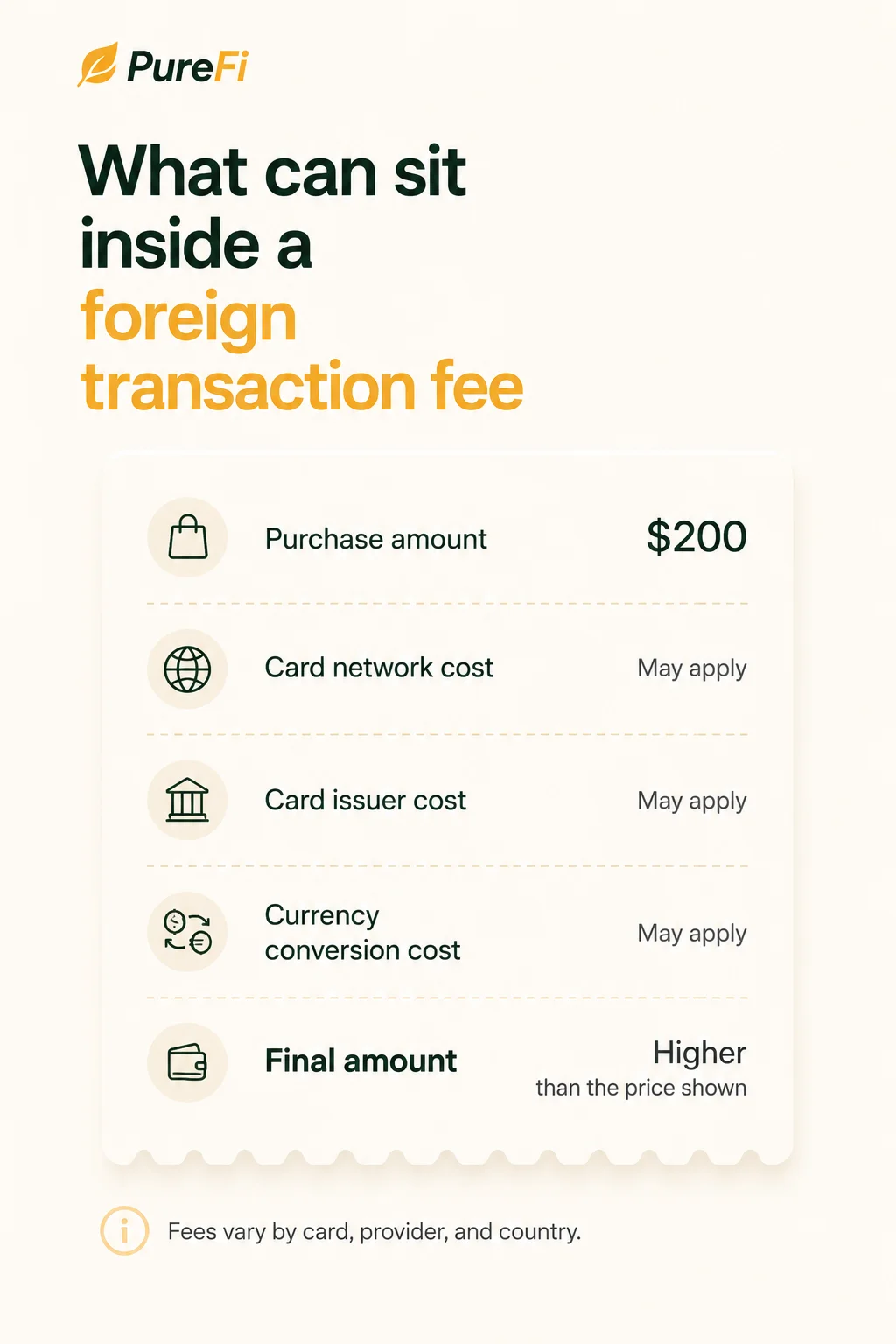

A typical foreign transaction fee can include two parts: a network fee and an issuer fee. The network fee is charged by the card network that helps process the transaction. The issuer fee is charged by the financial institution that issued the card.

Simply put, more parties may be involved when a payment crosses borders. Each one may add a cost. The issue is not only that fees exist. Some services do have real costs. The issue is that many people do not see the full cost until later.

Foreign transaction fee vs currency conversion fee

A foreign transaction fee and a currency conversion fee are related, but they are not the same.

| Fee type | What it means | Simple example |

|---|---|---|

| Foreign transaction fee | Extra charge for an international payment | Your card adds 3% on a foreign purchase |

| Currency conversion cost | Cost of changing one currency into another | You get a weaker exchange rate |

| ATM or payout charge | Extra charge from a local ATM or payout provider | The ATM adds its own withdrawal fee |

Sometimes more than one fee can apply to the same payment. That is why the final amount can be higher than expected.

Where foreign transaction fees show up

Foreign transaction fees can show up in more places than people expect. They can appear when you use your card at a shop, restaurant, hotel, or ATM while traveling. They can also appear when you shop from an international website, pay for an online subscription billed from another country, book flights or hotels through a foreign merchant, or pay for services in another currency.

They may also show up when people manage costs across countries. For example, someone may live in one country, support family in another, and pay bills or purchases in more than one currency.

How foreign transaction fees affect people who send money abroad

Foreign transaction fees are not the same as transfer fees. But the pain is similar. Both can make cross-border money use more expensive. For people who send money abroad, travel to see family, pay bills in another country, or shop internationally, these small charges can build up over time.

A $15 charge may not change much once. But again and again, it takes money away from things that matter. That is why we believe fees, exchange rates, and hidden fees should be easy to understand. People should be able to keep more of what they earn.

How to avoid foreign transaction fees

You can’t avoid every fee in every situation. But you can reduce surprises by checking the full cost before you pay.

Check your card fees before you travel

Before you use a card outside your country, check the card’s fee schedule or cardholder agreement. Look for foreign transaction fees, ATM withdrawal fees, and currency conversion charges. This small step can save you from finding out after the payment has already gone through.

Use cards made for international spending

Some cards are built for travel or international use and may charge no foreign transaction fee. Others may still charge one. Do not assume your card is cheaper because it has a good brand name. Check the actual fee.

Pay in the local currency when offered a choice

When you travel, a card machine or ATM may ask if you want to pay in your home currency or the local currency. Paying in your home currency may feel easier, but it can include extra conversion costs. Visa says dynamic currency conversion can include an exchange rate and additional fees.

In many cases, paying in the local currency gives your card provider the chance to use its own conversion rate. Still, always check your card terms.

Compare the exchange rate, not only the fee

A “no foreign transaction fee” card or service can still have a poor exchange rate. Before you send money abroad or pay across borders, look at the fee, the exchange rate, and the final amount. This is the best way to understand what it really costs.

Watch out for ATM charges

Foreign ATMs may charge their own fee. Your card provider may also charge a separate withdrawal fee. If you need cash while traveling, check whether your provider has partner ATMs or lower-cost withdrawal options in that country.

Why clear pricing matters

People should not need to read fine print after every payment. A fair payment tool should show what you are paying before you confirm. It should not hide the real cost inside rates, markups, or surprise charges.

At PureFi, we believe money should work for people, not against them. If someone is sending money abroad, paying a bill, or supporting family, they should know what they are paying from the start.

Conclusion

Foreign transaction fees are one of those charges people only notice after they’ve already paid. That is what makes them frustrating. The fee is not always large enough to stop a purchase, but it is large enough to take value away over time.

For people who live, travel, shop, or support family across borders, these small costs are part of a bigger issue. The traditional system often makes international money use harder and more expensive than it needs to be.

Better financial tools should make the cost clear from the start. No surprise charges, confusing rates, or guessing what happened after the payment goes through.

Get PureFi for money transfers

PureFi helps you send money abroad for less, with clear fees and a simple way to hold and grow your money. We use new technology to make cross-border transfers faster, fairer, and more transparent.

Learn more about how PureFi can help you send, save, and grow money across borders, or download the app to get started today.